Greenfield manufacturing is increasingly cross-border. Manufacturers are placing factories where the incentives, labor pools, and regulatory pathways favor their sector — semiconductors in the USA under CHIPS Act, industrial AI and power grids in Germany’s European corridor, automotive and sovereign-capital-backed ecosystems in the UAE. The right country choice can swing project economics by 30–50%, while the wrong regulatory pathway can add 6–12 months to schedule. iFactory’s global greenfield consulting practice combines country-specific regulatory expertise, labor market intelligence, and AI-powered project management to plan and execute factories across the USA, Germany, UAE, and global manufacturing hubs. Book a global greenfield strategy session to evaluate your country shortlist against current incentive and timeline reality.

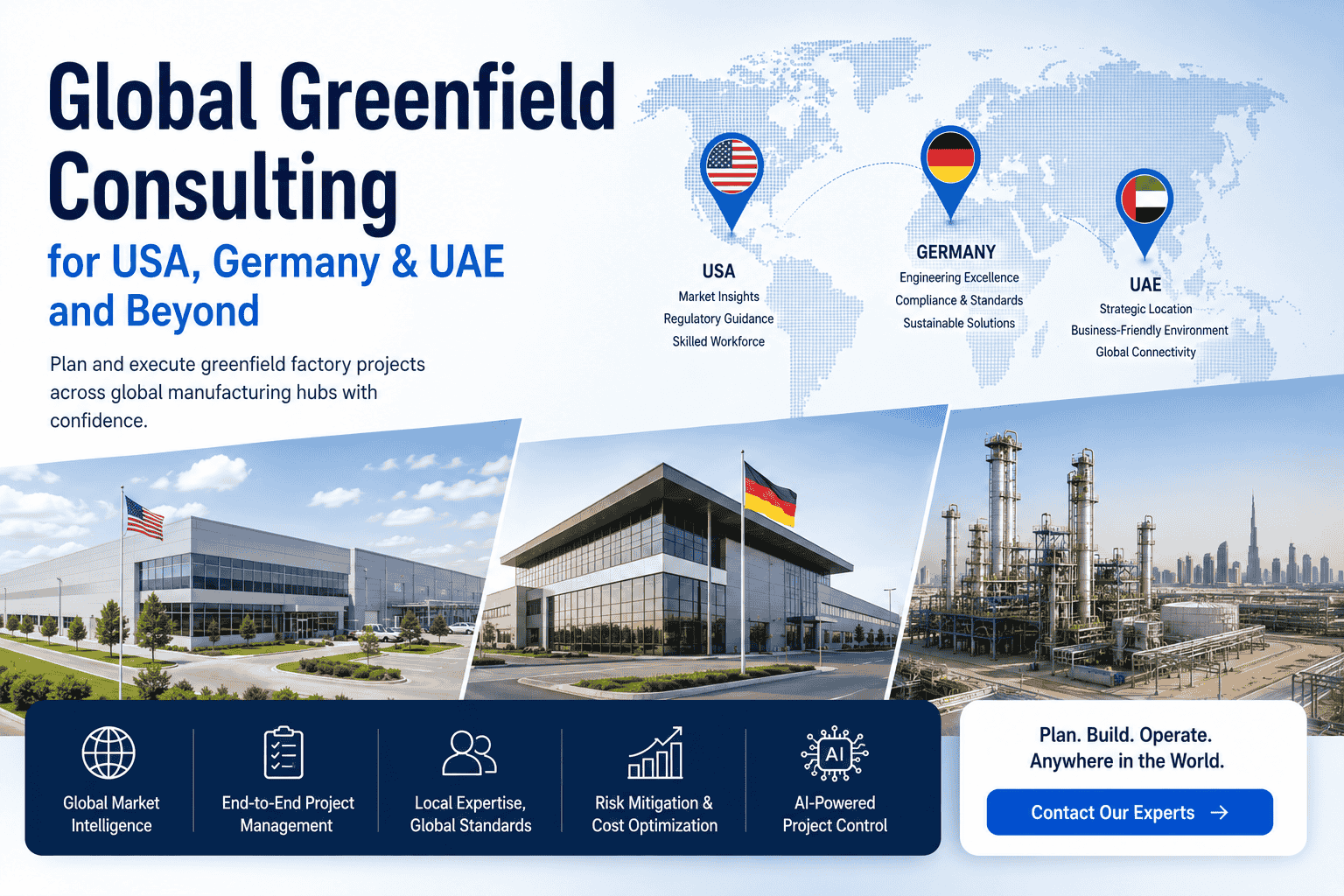

International Factory Planning & Execution

Greenfield Projects Across USA, Germany & UAE

Country-specific regulatory navigation, labor market intelligence, incentive negotiation support, and AI-powered project management. From site selection through ramp-up — in any of the three markets or coordinated across all of them.

$560B+US manufacturing megaproject investment committed

AED 40BUAE Ministry of Industry financing available

$270BAsia-Middle East corridor projected flows

Three Markets, Three Realities

USA

United States

CHIPS Act + IRA incentives

Texas semiconductor hub

12–24 mo standard timeline

DEU

Germany

European industrial corridor

Semiconductors & power grids

Sector collective agreements

UAE

United Arab Emirates

Made in Emirates incentives

Sovereign capital available

Dubai #1 greenfield city

Why Country Choice Drives 30–50% of Project Economics

Country selection isn’t a logistics decision — it’s a financial decision that compounds across the 3–5 year build and the 20-year operating life. Capital incentives shift by 10–30% of project value depending on jurisdiction. Labor costs and availability shift by 50–200% across regions. Regulatory timelines shift by 6–18 months. Tariff exposure shifts by 0–25% on imported components. The countries that look comparable on a spreadsheet diverge sharply once incentives, labor market reality, and regulatory pathways are mapped to your specific sector and product.

10–30%

Project value swing from capital incentives by jurisdiction

50–200%

Labor cost variance across regional manufacturing markets

6–18 mo

Regulatory timeline variance by country & sector

0–25%

Tariff exposure delta on imported components

2–4×

Energy cost variance across global manufacturing markets

$1.3B

Average overrun on megaprojects without country expertise

USA — Greenfield in the CHIPS & IRA Era

The United States has committed over $560 billion in manufacturing megaproject investment, anchored by the CHIPS and Science Act, the Inflation Reduction Act, and state-level incentives that can exceed $1.5 billion for individual projects (Rivian Georgia, Tesla Nevada, Samsung). Texas has emerged as the leading semiconductor and EV construction hub. The FDA’s PreCheck program (launched 2025) streamlines pharma approvals. But execution complexity is rising: skilled construction labor is constrained, project leadership talent is scarce, and federal incentives carry compliance requirements that compound the documentation burden.

Capital Incentives

CHIPS Act, IRA & State-Level Programs

CHIPS Act: billions in semiconductor build funding (Samsung received $4.7B)

IRA: $35/kWh production credits for battery cells

Rivian Georgia: $1.5B incentive package with job-creation thresholds

Tesla Nevada: $330M tied to semi-trucks & batteries facility

State-level workforce training grants stackable with federal incentives

Regulatory Pathway

EPA, OSHA, FDA & State Permitting

EPA permitting: 6–18 months depending on air, water, hazmat scope

FDA PreCheck (2025): streamlined pharma plant approvals

OSHA process safety management for chemical/petrochemical sites

State environmental review (CEQA in CA, similar elsewhere)

Local building & zoning approvals vary by jurisdiction

Labor Market

Construction & Operations Talent

Skilled construction labor: severe shortage in 2026 megaproject regions

Semiconductor project managers: aggressive cross-recruiting among firms

Texas leading hub: lower costs, business-friendly environment, scale

Sign-on bonuses, retention packages, relocation now standard

Right-to-work states preferred for compressed delivery timelines

Sector Focus

Where US Greenfield Is Concentrating

Semiconductors: Micron (Clay NY), Samsung, Intel expansion projects

EV & battery: Rivian Georgia, gigafactory wave nationwide

Pharmaceuticals: domestic API capacity, FDA PreCheck enabled

Advanced manufacturing: defense electronics, aerospace components

Data centers: AI infrastructure driving power-led site selection

Planning a US greenfield in semiconductors, EV, or pharma? Book a strategy session — we map CHIPS/IRA eligibility, state incentive stacking, and Texas vs. coastal state economics for your specific scope.

Germany — The European Industrial Corridor Anchor

Germany anchors a new European industrial corridor with France and the Nordics, attracting greentech, semiconductor, and industrial AI investment at scale. The country’s strategic refocus on semiconductors, power grids, and industrial AI creates opportunity for foreign manufacturers entering the European market through German production. The challenge isn’t capital or technology — it’s talent: Germany’s workforce transition from traditional manufacturing roles to high-tech specialists (systemic integrators who bridge physical machines and digital simulation) is the binding constraint on most 2026 projects.

Strategic Position

European Industrial Corridor Anchor

Anchors corridor with France (regulatory navigation) and Nordics (deep tech)

Refocus on semiconductors, power grids, industrial AI in 2026

Largest EU economy with mature supplier ecosystem

Direct access to EU single market without import tariffs

Strong existing greentech and advanced manufacturing base

Regulatory Pathway

German & EU Compliance Framework

Federal Immission Control Act (BImSchG) for industrial permits

EU Carbon Border Adjustment Mechanism (CBAM) compliance

Länder-level (state) variation in approval timelines

Environmental Impact Assessment (UVP) for major projects

EU machinery directive compliance for installed equipment

Labor Reality

Workforce Transition Challenge

Workforce shifting from traditional mfg to high-tech roles

Systemic integrators (machines + simulation) in highest demand

Sector-level collective agreements (IG Metall) must be navigated

Works councils (Betriebsrat) require structured engagement

Skilled trades pipeline strong but competing with EV transition

Sector Focus

Where German Greenfield Is Concentrating

Semiconductors: Intel Magdeburg, ESMC (TSMC) Dresden announcements

Battery & EV: gigafactory cluster across northern & eastern regions

Industrial AI: integration into existing automotive supplier base

Power grid components: anchoring European energy transition

Pharma & biotech: established mid-tier production capacity

Map Your Country Shortlist Against 2026 Reality

A strategy session evaluates 2–3 country candidates against your specific sector, capital plan, and timeline constraints. You leave with a documented country comparison covering incentives, regulatory timelines, labor availability, and key 2026 risk factors.

UAE — Sovereign Capital & the Made in Emirates Era

The United Arab Emirates has positioned itself as a global manufacturing destination with sovereign capital availability, energy cost advantages, and the Made in Emirates campaign. Dubai ranks #1 globally for greenfield city attractiveness. The Ministry of Industry and Advanced Technology signed agreements providing AED 40 billion (USD 10.9B) in competitive financing over five years. Abu Dhabi Investment Office targets AED 8 billion (USD 2.2B) in FDI for the automotive value chain. The Asia-Middle East corridor is projected at $270 billion in flows. The UAE plays differently than USA or Germany — it requires localization strategy and regional HQ positioning, not just factory siting.

Capital Access

Sovereign Capital & Industry Financing

AED 40B (USD 10.9B) Ministry of Industry competitive financing

Abu Dhabi Investment Office automotive ecosystem FDI program

Mubadala, ADQ, ADIA sovereign wealth fund partnerships available

Made in Emirates campaign procurement opportunities

Free zone vs mainland entity structure decisions affect capital flow

Strategic Position

Global Manufacturing Hub

Dubai #1 globally for greenfield city attractiveness

Asia-Middle East corridor with $270B projected flows

Energy cost advantages vs Western markets

Free zones (JAFZA, KIZAD, RAKEZ) with 0% corporate tax structures

AI partnerships multiplying (Microsoft-G42 anchor)

Regulatory Pathway

UAE Compliance Framework

Federal industrial licensing through Ministry of Industry

Emirate-level approvals (Dubai DET, Abu Dhabi DED, etc.)

Free zone authority structure differs from mainland

Localization (Emiratization) requirements scaling annually

Environmental approvals through emirate-level agencies

Sector Focus

Where UAE Greenfield Is Concentrating

Automotive ecosystem: Abu Dhabi $2.2B FDI target

AI infrastructure: G42 partnerships, data center buildout

Pharmaceuticals: regional manufacturing for GCC distribution

Petrochemicals: integration with existing energy infrastructure

Aerospace & defense: Strata, EDGE Group expanding

How iFactory’s Global Practice Works

iFactory’s global greenfield practice combines four capabilities that conventional management consultancies and EPC firms handle separately. The integrated approach means country selection feeds directly into regulatory pathway planning, which feeds labor market analysis, which feeds AI-powered project management — all under a single accountable team rather than three or four firms exchanging documents.

01

Country Strategy & Site Selection

Multi-country evaluation against your specific sector, capital plan, and timeline. Incentive stacking analysis (federal + state + local). Labor market depth modeling. Energy and infrastructure capacity verification. Sovereign capital pathway mapping (UAE) and federal program eligibility (USA/Germany).

02

Regulatory Pathway Navigation

Country-specific regulatory expertise: EPA/OSHA/FDA in USA, BImSchG/CBAM/UVP in Germany, Ministry of Industry/free zone authority in UAE. Permit pathway prediction, environmental approval timelines, and stakeholder engagement strategy. Compliance gating integrated into project schedule.

03

Labor Market Intelligence

Construction labor availability in target regions (severe US shortage, transitioning German workforce, expat-heavy UAE pool). Operations labor planning. Compensation benchmarking. Sector collective agreement navigation (Germany IG Metall, US union vs right-to-work). Emiratization compliance planning (UAE).

04

AI-Powered Project Management

iFactory’s risk intelligence platform layers above your EPC partner and PM software. AI monitoring across procurement, design, regulatory, and execution risks. Probability-weighted alerts when variance crosses threshold. Country-aware models tuned to USA, German, and UAE regulatory and supply chain patterns.

Country Comparison at a Glance

The three markets favor different sectors, different capital structures, and different operational models. Use this comparison as a starting point — full strategy sessions tune the analysis to your specific sector, capital availability, and timeline constraints.

← Swipe to see all columns →

Need a country comparison tuned to your specific sector and capital plan? Book a strategy session — the comparison gets customized to your real project economics, not generic averages.

Deployment Timelines by Sector

Build timelines vary by sector more than by country. Food processing facilities go up in months; semiconductor fabs take years. Plan your country shortlist with realistic sector timelines, not generic averages — the difference between an 18-month battery plant and a 5-year pharmaceutical facility changes which incentive programs apply and which regulatory pathways gate the schedule.

Food Processing

3–7 months

Metal-building construction, equipment install, validation. Fastest greenfield category.

Standard Manufacturing

12–24 months

Discrete and process manufacturing. Most common build profile across sectors.

Automotive Assembly

2–4 years

Paint shop, body shop, assembly, supplier park. Complex robotic commissioning.

Pharmaceutical/Biotech

3–5 years

Includes GMP qualification, FDA/EMA approval cycles, cleanroom commissioning.

Semiconductor Fab

3–5 years

Cleanroom buildout, 24–36 mo equipment lead times, utility capacity buildout.

Battery Gigafactory

2–3 years

Process scale-up, supplier ecosystem, IRA $35/kWh production credits gating.

Industries iFactory Serves Globally

iFactory’s global greenfield practice covers six manufacturing sectors with sector-specific regulatory and operational expertise. The country-by-country specifics adapt to where your project lands — FDA PreCheck in USA, EMA in Europe, MOH UAE in the Emirates — but the sector framework stays consistent so your team isn’t reorienting for each country shortlist evaluation.

Food & Beverage

FSMA 204 (USA), EFSA (EU), MOH (UAE) compliance. CIP cycle validation, allergen controls, hygienic equipment specification. Fastest country-to-country deployment patterns.

Pharmaceuticals

FDA PreCheck (USA), EMA (EU), MOH UAE regulatory pathways. GMP qualification, cleanroom commissioning, validated workflow gating. 3–5 year build profiles.

Automotive & EV

Gigafactory wave (USA), European corridor (Germany), Abu Dhabi automotive ecosystem (UAE). IRA $35/kWh credits, supplier qualification, paint shop environmental approvals.

Semiconductors

CHIPS Act (USA), Intel/TSMC corridor (Germany), G42 partnerships (UAE). Cleanroom buildout, 24–36 mo equipment lead times, utility capacity verification.

Chemicals & Petrochem

EPA Title V (USA), BImSchG (Germany), MOIAT (UAE). Process hazard analysis, hazmat storage compliance, environmental remediation, sovereign energy integration (UAE).

Industrial AI & Data Centers

Power-led site selection, fiber connectivity, edge computing infrastructure. Microsoft-G42 partnership template in UAE, hyperscaler patterns in USA, European corridor industrial AI.

Plan Your Greenfield Across USA, Germany & UAE

A 60-minute strategy session evaluates your country shortlist against current 2026 incentive reality, regulatory timelines, and labor market constraints. You leave with documented country recommendations tuned to your sector, capital plan, and target go-live date. No engagement commitment required to participate.

Frequently Asked Questions

We’re early in country selection — can iFactory help us shortlist before we commit?

Yes — country shortlisting is the most common entry point for iFactory’s global greenfield practice. The strategy session evaluates 2–3 candidate countries against your specific sector, capital plan, target product mix, and timeline. We map current 2026 incentive eligibility (CHIPS/IRA in USA, EU/Länder programs in Germany, AED 40B Ministry of Industry financing in UAE), regulatory timelines, labor market constraints, and energy/infrastructure capacity. Output is a documented country comparison your executive team can use to make the commit decision. Many engagements stop here — clients select a country and execute internally — and that’s a fine outcome.

Do you work outside USA, Germany, and UAE?

Yes. The three named markets are our deepest-coverage regions, but the practice extends to global manufacturing hubs including India, Mexico, Vietnam, Malaysia, Saudi Arabia, France, Poland, and Brazil. Sector regulatory frameworks (FDA, EMA, FSSAI, ANVISA, etc.) and labor market patterns vary, but the underlying greenfield methodology stays consistent. If you’re evaluating a market not listed, the strategy session still applies — we’ll be transparent about coverage depth in your specific country candidates and whether local partners need to augment the engagement.

How does this differ from a Big Four management consulting engagement?

Three differences. First, integration: iFactory combines country strategy, regulatory pathway, labor intelligence, and AI-powered project management under one accountable team. Big Four engagements typically separate these into different practice areas with different leads. Second, technology: iFactory’s AI risk intelligence platform monitors project execution continuously, not just produces reports at milestones. Third, specialization: iFactory focuses exclusively on greenfield manufacturing, so the methodology, country relationships, and sector benchmarks are deeper than at generalist firms. The trade-off: Big Four firms may have broader brand recognition for board presentations. Some clients use both — iFactory for execution depth, Big Four for board-level validation.

Can you coordinate a project that spans multiple countries simultaneously?

Yes — multi-country greenfield coordination is increasingly common as manufacturers build regional production networks. A typical example: a battery manufacturer building one US gigafactory under IRA, one German facility for European market access, and one UAE plant for Asia-Middle East corridor distribution. iFactory coordinates the three projects with shared methodology, consistent AI risk monitoring, and country-specific regulatory leads. Schedule alignment, capital allocation phasing, and supplier coordination across the three projects gets managed centrally. This pattern is harder for firms with single-country focus and easier for global EPCs (Fluor, Bechtel, Jacobs) — iFactory complements those EPCs with the country strategy and AI risk monitoring layers they don’t typically provide.

What kind of capital are typical greenfield projects in these markets?

Range varies dramatically by sector and country. Food processing facilities typically run $20–100M. Standard manufacturing $50–300M. Automotive assembly $1–5B (Rivian Georgia is $5B). Pharmaceutical plants $200M–2B (including validation). Semiconductor fabs $5–20B (Samsung, TSMC scale). Battery gigafactories $2–5B (Tesla Nevada $3.6B). iFactory’s practice covers the full range — the methodology scales because the underlying greenfield framework stays consistent even as the capital and timeline grow. For mega-projects ($1B+), the working session typically expands to a 2–3 day workshop with executive sponsors, EPC candidates, and country incentive negotiators in the room together.

Is the strategy session a sales pitch or actual analysis?

Actual analysis. The 60-minute strategy session walks through your specific country shortlist with iFactory’s methodology applied live — not a generic capability pitch. Sessions typically include your project sponsor, CFO or finance lead, and operations or supply chain leadership. iFactory’s global greenfield lead facilitates. You leave with documented country recommendations, identified critical decisions, and a clear path forward whether that involves engaging iFactory or executing internally. No engagement commitment required to participate; we recover session value through subsequent engagements when there’s good fit, not by gating insight behind sales calls.