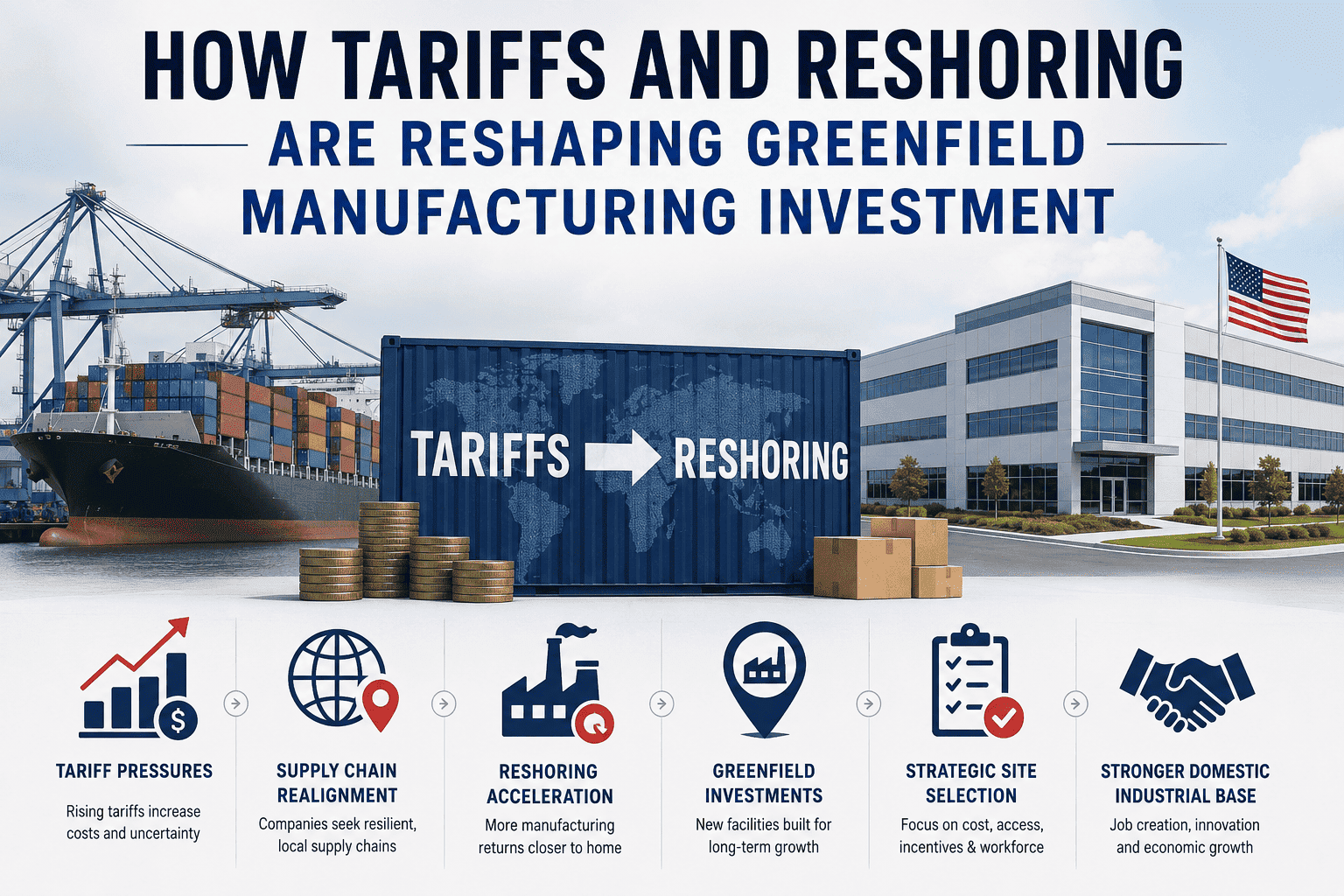

How Tariffs and Reshoring Are Reshaping Greenfield Manufacturing Investment

By Riley Quinn on June 9, 2026

In April 2025, the White House declared "the largest reshoring wave in American history." Major manufacturers responded almost immediately — Johnson & Johnson announced $55 billion in U.S. facility investments, Stellantis committed $13 billion, GlobalFoundries pledged $16 billion for domestic chip manufacturing. Over $3 trillion in reshoring investments have been announced in the U.S. since early 2025. The message from trade policy is clear: build here, or pay the tariff. But the real story for executives designing greenfield facilities is more complex than the headlines suggest. Tariffs are reshaping where factories get built, why they get built and how fast they need to be operational — and the manufacturers who understand the full picture are making better decisions than those reacting to the news cycle.

The Reshoring Investment Landscape — 2025–2026

$3T+

Reshoring investments announced in the U.S. since early 2025

iFactory Greenfield Research

96%

of manufacturers satisfied after reshoring to the U.S.

Reshoring Initiative, 2025

64%

of manufacturers not planning to reshore despite tariff pressure

ISM Survey, 2025

5.6%

Increase in U.S. manufacturing construction spending Feb 2025–Mar 2026

IoT Analytics, 2026

The Real Reshoring Equation: What's Driving Investment and What Isn't

Tariffs are the trigger, but they're rarely the full investment thesis. The manufacturers making the largest and most durable greenfield commitments in 2025–2026 are responding to a convergence of pressures — not just tariff avoidance. Understanding the full driver mix is essential before committing to a site or a construction timeline.

What's Actually Driving the Greenfield Decision

Supply chain localization (proximity to customers/engineering)

~48%

Primary

Lower freight and duty costs

~48%

Primary

Geopolitical risk reduction (China decoupling)

~38%

Major

Government incentives (CHIPS Act, tax credits, grants)

~34%

Major

Tariff avoidance (direct policy response)

~27%

Secondary

Energy availability and cost stability

~24%

Secondary

Workforce availability for advanced manufacturing skills

~19%

Secondary

Source: Reshoring Initiative 2025 Survey (500+ manufacturers). Percentages indicate portion of respondents selecting as primary or major factor.

Evaluating whether a greenfield investment makes sense for your business? Book a Greenfield Consultation — iFactory's team analyzes your full driver mix before any site commitment is made.

The Three Investment Paths: Reshore, Nearshore, or Friendshore?

Not every manufacturer facing tariff pressure has the same optimal response. The decision between building in the U.S., building in a lower-cost but geopolitically aligned neighbor (Mexico, Canada), or diversifying to a "friendshore" partner country (Vietnam, India, Poland) depends on product type, supply chain structure, labor intensity, capital availability, and expected policy durability. Here's how to think through the three paths.

Reshoring

Build in the U.S.

Best for:

Semiconductors, defense, pharma — strategic sectors with CHIPS/IRA incentives

Products where customer proximity drives premium pricing

Capital-intensive, automation-heavy operations where U.S. labor cost premium is mitigated

Watch out for:

Construction timelines 40–60% longer than Asian builds. Skilled workforce gaps — nearly 500,000 unfilled advanced manufacturing jobs. High operating costs still 30–50% above comparable Asian facilities without full automation offset.

SemiconductorsPharmaDefenseEV Batteries

Nearshoring

Build in Mexico / Canada

Best for:

Labor-intensive assembly operations where U.S. cost premiums are prohibitive

Time-sensitive supply chains where 2-day truck access to U.S. customers matters

Watch out for:

USMCA rules-of-origin compliance complexity. Mexico political risk and infrastructure variability by region. Nearshored facilities may still face tariff exposure if supply chain inputs aren't localized adequately.

AutomotiveAppliancesElectronicsConsumer Goods

Friendshoring

Build in Allied Nations

Best for:

Global supply chains that serve multiple end markets — not just North America

China+1 strategies — Vietnam, India, Poland offer lower cost with geopolitical alignment

Categories where cost discipline is non-negotiable but China sourcing is no longer viable

Watch out for:

Tariff-exposed sectors (textiles, electronics, machinery) saw project numbers fall 25% in 2025. Geopolitical distance of greenfield FDI has shrunk 2× since 2017 — the window for true cost arbitrage is narrowing.

VietnamIndiaPolandMalaysia

Site Selection in the Tariff Era: The Factors That Now Matter Most

Site selection for greenfield manufacturing facilities has fundamentally changed. Decisions that were once dominated by labor cost comparisons now involve a multi-factor matrix where energy availability, infrastructure readiness, incentive packages, and supply chain proximity often outweigh pure wage arithmetic. Here's what the leading site selectors and corporate real estate teams are weighting in 2026.

#1

Energy Availability & Reliability

Rose to #1 in 2025–2026

Power availability has surpassed proximity to markets as the dominant site selection factor for advanced manufacturing and AI-intensive facilities. Grid reliability, available substation capacity, and path to renewable sourcing are now evaluated in the first screening round — not after shortlisting. Regions like Phoenix, Dallas-Fort Worth, and Salt Lake City are rising specifically because of energy infrastructure.

#2

Skilled Workforce Availability

Persistent constraint

Nearly 500,000 advanced manufacturing jobs remain unfilled in the U.S. because modern factories require digital, robotics, and AI skills that current training pipelines can't supply at scale. Site selectors now evaluate community college partnerships, apprenticeship programs, and regional STEM pipeline depth alongside traditional labor cost metrics.

#3

Incentive Package & Total Cost of Ownership

Decisive at short-list stage

State and local incentives — tax abatements, infrastructure grants, workforce training credits, utility rate guarantees — can represent $50–200M+ in value for a major manufacturing project. The South and Midwest remain top destinations due to pro-business policy environments, with Ohio, Texas, Tennessee, and South Carolina consistently ranking as top competitive sites.

#4

Supply Chain Proximity

Reshoring multiplier

A greenfield facility only captures the full tariff advantage if key inputs and sub-assemblies are also domestic or USMCA-compliant. Sites near established supplier ecosystems — automotive clusters in the Midwest, semiconductor supply chains in Arizona and Texas, life sciences corridors in New Jersey and North Carolina — reduce total supply chain exposure beyond just the final assembly tariff.

#5

Permitting Speed & Regulatory Environment

Speed-to-production critical

Tariff windows create urgency. A facility that takes 4 years to permit and build may open into a different trade policy environment than the one that justified the investment. States with pre-permitted industrial sites, streamlined environmental review processes, and single-window permitting coordination are capturing investment that slower-permitting states are losing to Mexico or Canada by default.

#6

Digital Infrastructure & Connectivity

New entrant 2025

AI-driven manufacturing requires fiber connectivity, edge compute co-location options, and cloud-to-plant latency specifications that simply weren't on site selection checklists five years ago. Communities investing in industrial-grade digital infrastructure are differentiating themselves meaningfully for the next wave of greenfield investment.

Turn Trade Policy Pressure Into Greenfield Advantage

iFactory's greenfield consulting team analyzes your full investment thesis — tariff exposure, site selection, incentive capture, supply chain localization, and facility design — so you build the right plant in the right place at the right time.

Sectors Leading the Reshoring Wave — and the Greenfield Opportunity in Each

Reshoring is not uniform across industries. The sectors seeing the largest and most durable greenfield investment share a common profile: high strategic sensitivity, meaningful tariff exposure, available government incentives, and supply chains that are genuinely viable to localize. Here's where the real construction activity is concentrated.

Sector

Investment Signal

Key Catalyst

Greenfield Readiness

Semiconductors

Very High

CHIPS Act grants + 25%+ tariffs on Chinese chips. TSMC, Samsung, Intel all constructing U.S. fabs.

EV & Battery

Very High

IRA tax credits + tariff exposure from China supply chain. Auto OEMs shifting entire battery lines domestic.

Life Sciences & Pharma

High

J&J $55B + $200B+ multi-year commitments. API supply chain from China/India identified as national security risk.

Section 232 steel tariffs + domestic content rules creating modest but meaningful new investment activity.

Consumer Electronics

Cautious

64% of affected manufacturers not reshoring — labor cost gap too wide. Nearshoring to Mexico or Vietnam more common.

The Hidden Cost Trap: Why Tariff-Justified Greenfield Projects Fail

Not every reshoring announcement becomes a completed, competitive factory. The manufacturers who make expensive greenfield mistakes in the tariff era share a common pattern: they justify the investment on tariff savings alone, without fully modeling the structural cost differences between U.S. and Asian operations. Understanding these gaps isn't pessimism — it's the analysis that separates successful greenfield projects from expensive lessons.

Construction Cost & Timeline Inflation

U.S. greenfield construction runs 40–60% more expensive than comparable Asian builds, and timelines routinely stretch to 3–5 years vs. 18–24 months elsewhere. A tariff that justified the ROI in Year 1 modeling may not sustain through a prolonged construction window — especially if trade policy shifts during build-out.

Input Cost Exposure — The Supply Chain Tariff Layer

Raw material prices increased 5.4% in 2025 and are projected up another 4.4% in 2026 — partly driven by tariffs on imported inputs. A final assembly operation reshored to the U.S. that still sources components from tariff-exposed countries inherits the cost without capturing the domestic content benefit. 86% of manufacturers are passing some of these costs to customers, but competitive pricing pressure limits how much can be passed through.

Workforce Skills Gap at Scale

Nearly 500,000 advanced manufacturing positions remain unfilled. Modern factories require digital operations, robotics programming, and AI system management skills that traditional manufacturing workforces don't have — and retraining pipelines haven't caught up. A greenfield facility that models full-capacity production in Year 2 without a concrete workforce development plan will miss targets.

Policy Duration Risk

A greenfield facility has a 20–30 year economic life. A tariff structure has a presidential cycle. Manufacturers who model their entire investment case on current tariff levels — without stress-testing for policy reversal — are taking a risk that site selectors and CFOs should explicitly quantify. The plants that survive trade policy swings are the ones with structural cost competitiveness, not just tariff protection.

Ready to stress-test your greenfield investment thesis? Schedule a greenfield investment review — iFactory models tariff scenarios, total cost of ownership, and 10-year ROI before you commit to a site.

Expert Perspective

"Structural costs remain high — U.S. labor, energy, and operational expenses still far exceed Asian competitors, making reshoring viable only with advanced automation and redesigned production models. Workforce gaps are slowing reshoring. Nearly 500,000 manufacturing jobs remain unfilled because modern factories require digital, robotics, and AI skills that current training systems can't supply at scale. Reshoring is real — but it succeeds only where the full picture is modeled."

— Supply Chain Management Review, Analysis of Tariff Era Reshoring, 2025

$200B+

Multi-year U.S. investment commitments announced in 2025 by major life sciences companies alone

52.7

ISM Manufacturing PMI in March 2026 — multi-year high signaling recovery

38%

of reshoring manufacturers cite geopolitical risk reduction as a primary driver

Conclusion: Build for Structure, Not Just for Tariffs

The manufacturers making the best greenfield decisions in 2026 are not the ones reacting fastest to tariff announcements. They're the ones building facilities that will be competitive under any plausible trade policy scenario — because they designed for automation density, supply chain integration, workforce development, and digital infrastructure from day one. Tariffs are an accelerant, not a foundation. The greenfield projects that will still be generating returns in 2035 are the ones that modeled total cost of ownership, chose sites based on the full six-factor matrix, and designed facilities capable of running with advanced manufacturing technology rather than just domestic labor substitution. iFactory's greenfield consulting team helps manufacturers do exactly that analysis — before a site is selected, before an architect is engaged, and before a dollar of capital is committed.

Make the Greenfield Decision with Complete Confidence

From tariff scenario modeling to site selection, supply chain localization, and AI-ready facility design — iFactory delivers the complete greenfield investment analysis before you commit capital. Start your consultation today.

Are tariffs actually causing a manufacturing reshoring boom in the United States?

The data shows a more nuanced picture than the headlines suggest. U.S. manufacturing construction spending increased 5.6% between February 2025 and March 2026, and major investment announcements — $55B from Johnson & Johnson, $16B from GlobalFoundries, $13B from Stellantis — are real. The ISM Manufacturing PMI hit a multi-year high of 52.7 in March 2026. However, 64% of manufacturers say they have no plans to reshore despite tariff pressure, primarily because U.S. construction and operating costs remain 30–50% higher than Asian alternatives without full automation offset. The honest assessment: reshoring is accelerating meaningfully in strategic, incentivized sectors — semiconductors, EV batteries, pharma, defense — but is not yet the broad manufacturing revival some headlines suggest.

What are the most important site selection factors for a greenfield manufacturing facility in 2026?

The site selection calculus has shifted significantly. Energy availability and grid reliability have risen to the top factor, surpassing even labor cost for AI-intensive and advanced manufacturing facilities. Workforce availability for digital and robotics skills, the size and structure of state and local incentive packages, supply chain proximity to domestic suppliers, permitting speed and regulatory environment, and digital infrastructure quality round out the top six factors. Traditional cost-per-square-foot analysis is now just one input in a multi-factor scoring model. Sites that win in 2026 offer strong energy infrastructure, a credible workforce development pipeline, and a competitive incentive package — and can demonstrate a realistic path from groundbreaking to production in under 36 months.

What is the difference between reshoring, nearshoring, and friendshoring — and how do I choose?

Reshoring means building in the United States — best for strategic sectors with government incentives (CHIPS, IRA) and for capital-intensive operations where full automation offsets the labor cost premium. Nearshoring means building in Mexico or Canada — best for labor-intensive assembly operations that benefit from USMCA tariff exemptions and proximity to U.S. customers while maintaining competitive labor costs. Friendshoring means building in geopolitically aligned countries (Vietnam, India, Poland, Malaysia) — best for global supply chains serving multiple markets where cost discipline is non-negotiable but China sourcing is no longer viable. The right choice depends on your product category, labor intensity, capital budget, end market geography, and realistic assessment of how durable current U.S. tariff levels are likely to be over your facility's 20-year investment horizon.

Which manufacturing sectors are seeing the most greenfield investment activity due to reshoring?

Semiconductors and EV batteries are leading — both combine high tariff exposure, massive government incentives (CHIPS Act, IRA), and supply chains where domestic localization is strategically viable. Life sciences and pharmaceuticals are seeing substantial activity driven by national security concerns about API supply chain concentration in China and India. Defense and aerospace have domestic-content requirements that make reshoring effectively mandatory for new capacity. Steel, appliances, and renewable energy equipment are seeing more modest but meaningful activity. Consumer electronics broadly remain difficult to reshore at competitive unit economics — nearshoring to Mexico or Vietnam is the more common response in that category.

How should greenfield manufacturers account for tariff policy uncertainty in their investment planning?

The core principle is designing for structural competitiveness, not just tariff protection. A greenfield facility with a 20–30 year economic life will operate through multiple trade policy cycles. The investment case should be stress-tested under at least three scenarios: current tariff levels maintained, significant tariff reduction or reversal, and escalation. Facilities that are competitive primarily because tariffs make imported alternatives expensive — but would be uncompetitive without them — carry inherent policy risk. The greenfield facilities that sustain returns through trade policy changes are the ones with genuine structural cost advantages from automation, supply chain integration, and operational efficiency. iFactory's greenfield analysis models all three scenarios as standard practice before any site recommendation is made.