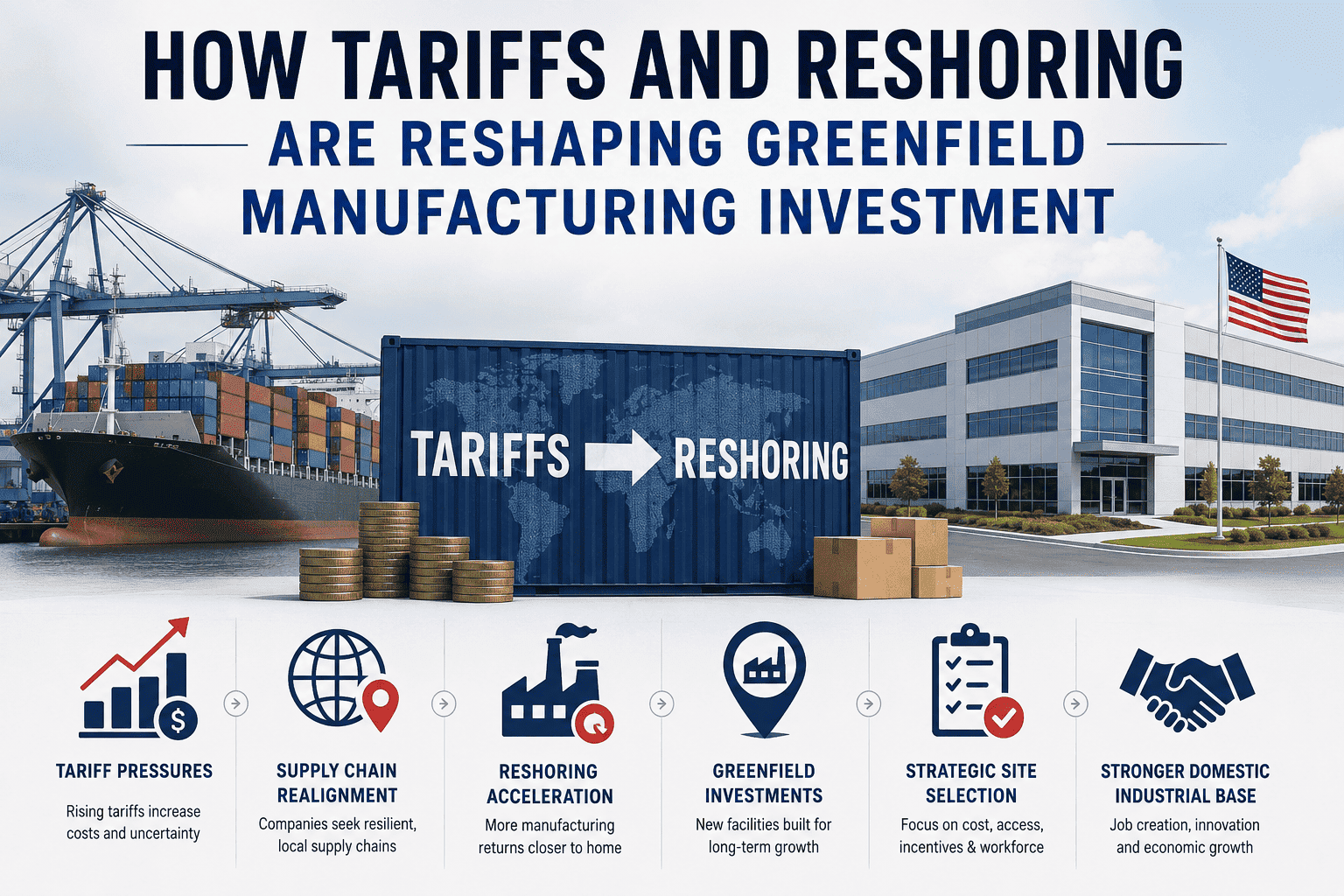

The Reshoring Initiative tracked 244,000 reshoring and FDI-announced manufacturing jobs in the United States in 2024, with Texas leading at 24,722 jobs across 125 cases — 11% of the national total. The CHIPS Act, Inflation Reduction Act, tariff environment, and post-pandemic supply chain re-evaluation have created the strongest case for US-based greenfield manufacturing in 30 years. But reshoring is not an overnight strategy. It involves site selection against six factors, workforce pipeline depth, utility lead times of 6 to 18 months, federal and state incentive stacking, FEED engineering for AI-native infrastructure, and total cost of ownership modeling that goes well beyond the labor-rate comparison that drove offshoring in the first place. The 15 considerations below are what separate a successful US reshoring greenfield from one that books the same overruns and ramp-up failures that plagued offshore builds. Book a US reshoring greenfield consultation to evaluate your site, incentive stack, workforce strategy, and total cost of ownership before land acquisition.

Top 15 Greenfield Plant Reshoring Considerations — US Manufacturers 2026

The Decisions That Separate a Successful Reshoring From an Expensive One

244K

Reshoring + FDI manufacturing jobs announced in 2024

Reshoring Initiative

11%

Of national reshoring jobs landed in Texas — top US destination

24,722 jobs across 125 cases

77%

Of OEMs cite geopolitical risk as a reshoring driver

IndustryWeek / Reshoring Initiative survey

67%

Of reshoring growth in semiconductors, EV batteries, solar & appliances

IRA + CHIPS Act-driven sectors

$725M

Caterpillar Lafayette IN investment — representative anchor commitment

Engine manufacturing capacity expansion

$2.65

Economic impact per $1 spent in US manufacturing — largest sector multiplier

National Association of Manufacturers

Track 1

Site Selection & Location Strategy

4 considerations

Track 2

Incentives & Capital Stack

3 considerations

Track 3

Workforce & Automation

4 considerations

Track 4

Engineering & TCO

4 considerations

Track 1 — Site Selection & Location Strategy

Texas led 2024 reshoring with 24,722 announced jobs, but the real story is that energy availability, workforce depth, supply chain proximity, and permitting speed have replaced land cost as the dominant site selection drivers. A low-cost site without grid capacity to support an AI-native plant becomes the most expensive site once delays compound through commissioning.

01

Energy Availability & Grid Reliability

Now the #1 site factor for advanced manufacturing. AI-native plants require 2-3x the electrical capacity of traditional facilities. Grid interconnect studies take 6 to 18 months.

Action: Request grid capacity letters from utility before land option is taken — not after.

02

Workforce Depth in the Local Market

2025 Reshoring Survey found a stronger skilled workforce would bring back more manufacturing than tariffs, weaker dollar, or lower taxes. The incentive package doesn't matter if the engineering pipeline isn't there.

Action: Talent market analysis with controls, process, plant leadership candidate availability before site selection.

03

Supply Chain & Customer Proximity

The risk premium of six-week ocean shipping has tipped the math in favor of domestic production. Proximity to tier 1 customers and key input suppliers now a structural advantage worth measuring.

Action: Map tier 1 customer locations and input supplier geography against site shortlist.

04

Permitting Speed & Regulatory Environment

Permit timelines vary significantly by state. Environmental clearances, zoning, and building permits can stall projects for weeks to months. State-level industrial readiness is now a measurable site selection factor.

Action: Pre-engage regulatory consultants in target jurisdictions; pursue parallel permitting tracks.

Track 2 — Incentives & Capital Stack

Federal incentives at a scale nobody expected — CHIPS Act funding flowing to semiconductor fabs, IRA credits pulling EV battery and clean energy manufacturing stateside, and state-level packages competing aggressively for major projects. The capital stack a 2026 reshoring greenfield assembles is fundamentally different from any prior decade. Number of firm cases citing Government Incentives is down 54% from 2024 while Tariff citations are up 454% — reflecting that incentives still matter but tariffs now drive more decisions.

Layer 1 — Federal Programmes

CHIPS & Science Act — Semiconductor fab funding, R&D credits, manufacturing investment tax credit

Inflation Reduction Act (IRA) — Clean energy manufacturing credits, EV battery, solar, advanced manufacturing

100% Bonus Depreciation — Accelerated equipment cost recovery, restored in current legislation

Refundable Tax Credits — Section 48C, Section 45X advanced manufacturing production credits

Layer 2 — State Programmes

Property tax abatements — 10 to 20 year structures common for anchor manufacturing investments

Job creation tax credits — Per-employee credits scaled to wage and skill level

Training grants — State workforce development funding for hire-and-train programmes

Infrastructure grants — Road, rail, utility connection, water/wastewater contributions

Layer 3 — Local & Utility

County / city packages — Land contributions, fee waivers, local property tax abatements

Utility incentives — Reduced electric rates, infrastructure cost-share, gas pipeline contributions

Foreign Trade Zones — Duty deferral and reduction on imported components

05

Federal Incentive Stacking Strategy

CHIPS Act, IRA Section 48C and 45X credits, bonus depreciation. Each programme has eligibility requirements, sourcing rules, and timing constraints that interact. Stacking errors leave money on the table.

Action: Tax and incentives counsel engaged before site selection — programme eligibility shapes site decisions.

06

State & Local Incentive Negotiation

States compete aggressively for anchor manufacturing. Property tax abatements, job credits, training grants, and infrastructure contributions are negotiable for projects above critical thresholds.

Action: Run competitive site selection with 3 to 5 finalist states to maximise leverage.

07

Tariff Exposure & FTZ Strategy

Tariff citation as reshoring driver up 454% in 2025. Foreign Trade Zone designation can defer or eliminate duties on imported components — increasingly meaningful with current tariff structures.

Action: Model component sourcing under current and likely future tariff scenarios; evaluate FTZ designation.

Need a federal + state + local incentive stack modeled against your sourcing profile? Book a reshoring consultation — we will produce the incentive analysis before land acquisition.

Track 3 — Workforce & Automation Strategy

The single most cited concern from 600 manufacturing executives in Deloitte's 2025 survey was equipping workers with skills for smart manufacturing. Immigrant workers filled nearly one in four US manufacturing production jobs in 2024 — shifting immigration policies are creating additional labor pool uncertainty. The successful reshoring play is automation-first: design for fewer, more highly skilled operators rather than competing for low-cost labor that does not exist in the US market at the volumes traditional plants required.

08

Automation-First Workforce Model

Design the plant for 40 to 60% fewer headcount than equivalent offshore facility through robotics, AI, and digital twin operations. Fewer, more highly skilled operators rather than competing for unavailable lower-skill labor.

Action: Automation roadmap and headcount model in FEED — not added after launch.

09

Skilled Talent Pipeline Building

The people who matter most for controls, process engineering, and plant leadership are not on job boards. Reshoring plants need 18 to 24 months of relationship building before key hire dates.

Action: Begin candidate sourcing for controls, process engineering, plant leadership at FEED — not at construction.

10

Training & Apprenticeship Programmes

Virginia, Ohio, and other reshoring-active states have built strategic education, hands-on training, and apprenticeship programmes. Partnership with state workforce development matters for both talent and incentives.

Action: Partner with state and regional workforce programmes during site selection, not after launch.

11

AR Wearables & Connected Worker Platforms

AR smart glasses, connected PPE, and worker copilots reduce training time 30 to 50% and accelerate ramp-up. Critical for new-hire-heavy reshoring plants where everyone is learning at once.

Action: Network coverage, edge compute, and AR platform specification in FEED for day-one deployment.

Design Your Reshoring Greenfield Around US Workforce Reality & Incentive Stack

iFactory's US reshoring consultation covers site selection against the 6 dominant factors, federal and state incentive stack modeling, workforce pipeline building, automation strategy that reduces required headcount, AI-native engineering, and total cost of ownership analysis — delivered before land acquisition.

Track 4 — Engineering & Total Cost of Ownership

The labor-rate comparison that drove offshoring two decades ago is no longer the right model for the reshoring decision. Total cost of ownership in 2026 must include tariff exposure, supply chain resilience cost, automation-enabled headcount reduction, energy cost, federal and state incentive recovery, IRA / CHIPS credit value, and the strategic option value of being close to customers. Plants reshoring based only on tariff savings produce different decisions than plants reshoring based on full TCO. The full-TCO plants are the ones that survive when the tariff environment changes.

12

Utility Lead Time Planning

Power, gas, water, and data connections to undeveloped land can take 6 to 18 months depending on local infrastructure capacity. Utility lead time is now consistently on the critical path of US greenfield projects.

Action: Utility connection studies parallel with site option period; commitment letters before financial close.

13

AI-Native Engineering at FEED

10 to 18% of CapEx for IT/OT infrastructure (vs 5 to 8% traditional) covers edge compute, private 5G or Wi-Fi 6E, unified data architecture, CMMS/MES, and cybersecurity. Retrofitting costs 4 to 6x more.

Action: IT/OT budget set at 10 to 18% at FEED; data architecture designed in.

14

Full Total Cost of Ownership Model

TCO must include tariff exposure, supply chain resilience value, automation-enabled headcount, energy cost, incentive recovery, customer proximity option value. Labor-rate-only comparison is the offshoring decision repeated.

Action: Full TCO model with sensitivity analysis on tariff and energy scenarios before site selection finalised.

15

Net-Zero & ESG Design From Day One

Customer Scope 3 reporting requirements cascading to suppliers. Net-zero design is increasingly a permitting and customer condition rather than a marketing item. Retrofit cost is multiples of greenfield.

Action: Solar, BESS, energy recovery, water reuse, and emissions metering specified at FEED.

Expert Perspective: The Reshoring That Works vs. The Reshoring That Disappoints

The US reshoring projects we audit at 18 months in fall into two distinct categories. The first group built their business case on tariff savings alone. When the tariff environment shifts — and it does — their economics break. They struggle to attract talent because labor costs are above offshore comparison. They run conventional automation density because that was the offshore model. They retrofit AI infrastructure post-launch at multiples of greenfield cost. The second group built the business case on full total cost of ownership — supply chain resilience, customer proximity, IRA and CHIPS Act incentive recovery, automation-enabled headcount reduction, energy cost stability, and the strategic option value of being able to respond to customer demand changes in 30 days rather than 6 months. These plants are profitable across multiple tariff scenarios. They attract talent because they are designed as modern AI-native facilities. They run 40 to 60% lower headcount than equivalent offshore plants through automation designed in from FEED. The decision is not whether to reshore — for many product categories that decision has already been made by the tariff and supply chain risk environment. The decision is whether to reshore well or reshore badly. The 15 considerations in this guide are the line between the two.

— iFactory Greenfield Consulting, US Reshoring Practice 2025 to 2026

$106,691

Average US manufacturing wage + benefits in 2024

4.8

Workers added to broader economy per US manufacturing worker

2M+

Reshoring jobs announced since 2010 — ~1.7M actually filled

Ready to design a US reshoring greenfield that survives multiple tariff scenarios? Talk to our US reshoring team — we will produce the full site, incentive, workforce, and TCO analysis before land acquisition.

Reshore Well — Not Just Reshore

iFactory's US reshoring greenfield consultation covers site selection scoring against energy, workforce, supply chain, and permitting factors, federal CHIPS / IRA / Section 45X incentive stack modeling, state and local incentive negotiation strategy, automation-first workforce design, AI-native IT/OT engineering, utility lead-time critical path planning, full TCO analysis with tariff and energy sensitivity, and net-zero ESG integration — all delivered before land acquisition or financial close.

Frequently Asked Questions

Which US states are leading reshoring greenfield investment in 2026?

Texas led 2024 with 24,722 announced reshoring and FDI jobs across 125 cases — 11% of the national total. Beyond Texas, the active reshoring states share a common profile: substantial available industrial land, energy grid capacity, organised workforce development programmes, and aggressive state-level incentive packages. Virginia and Ohio have built strategic education, hands-on training, and apprenticeship programmes that have become a meaningful site selection factor. Indiana attracted Caterpillar's $725 million Lafayette engine manufacturing investment. The Southeast generally and Gulf Coast specifically have benefited from chemical and petrochemical reshoring driven by CHIPS Act adjacency and energy availability. State leadership is genuinely competitive — companies running 3 to 5 finalist states typically extract meaningfully better incentive packages than single-state evaluations.

How do CHIPS Act and IRA incentives actually stack for a manufacturing greenfield?

Federal incentives stack across multiple layers. The CHIPS & Science Act provides semiconductor fab funding, R&D credits, and the Advanced Manufacturing Investment Credit (CHIPS ITC). The Inflation Reduction Act provides Section 48C Advanced Energy Project Credit, Section 45X Advanced Manufacturing Production Credit for components like solar cells, wind turbines, batteries, and critical minerals, plus restored 100% bonus depreciation for eligible equipment. State property tax abatements, job creation credits, training grants, and infrastructure contributions stack on top. Local utility and Foreign Trade Zone designations add further layers. Each programme has eligibility requirements, sourcing rules, prevailing wage and apprenticeship conditions, and timing constraints that interact. Stacking errors leave 5 to 20% of available incentive value unclaimed. Tax and incentives counsel engaged before site selection produces materially better outcomes than after.

Will US labor costs make reshoring uncompetitive even with incentives and tariffs?

The labor-rate comparison that drove offshoring two decades ago is no longer the right framing. US manufacturing wages averaged $106,691 including benefits in 2024 — meaningfully above most offshore alternatives on per-hour basis. But successful reshoring plants design for 40 to 60% lower headcount than equivalent offshore facility through robotics, AI, digital twin operations, and AR-enabled worker copilots. Combined with tariff savings, supply chain resilience value, energy cost stability, IRA / CHIPS incentive recovery, customer proximity option value, and the strategic value of 30-day demand response vs 6-month ocean lead time, full TCO comparison frequently favors US domestic production even at higher per-worker cost. The plants that struggle are the ones that reshored with the offshore automation density — competing on labor cost they cannot win. The plants that succeed reshored with automation-first design that turns the headcount equation into a strategic advantage.

What is the realistic timeline for a US reshoring greenfield from decision to production?

A US reshoring greenfield typically takes 3 to 5 years from strategic evaluation to full production capacity. The breakdown is: Strategy and Site Selection (6 to 12 months including incentive negotiation), FEED Engineering (6 to 12 months), Permitting and Site Preparation running parallel (4 to 8 months), Construction (12 to 30 months), Commissioning (4 to 9 months), and Ramp-Up to design capacity (6 to 12 months). Utility connections to undeveloped land are now consistently 6 to 18 months and frequently on the critical path. Permit pathway varies dramatically by state and project type — environmental clearances, building permits, and air permits can stall projects for weeks to months. Long-lead equipment procurement (transformers 18 to 24 months, custom vessels 12 to 18 months, specialised switchgear 14 to 16 months) must run in parallel with FEED at approximately 70% completion to avoid becoming the schedule bottleneck.

How does iFactory's US reshoring greenfield consultation actually work?

iFactory's US reshoring consultation covers your facility scope and product portfolio, target market geography and customer proximity analysis, site selection scoring across 6 factors (energy, workforce, supply chain, permitting, incentives, digital infrastructure), federal CHIPS / IRA Section 48C and 45X incentive stack modeling against your sourcing profile, state and local incentive negotiation strategy with 3 to 5 finalist states, workforce pipeline analysis with controls and process engineering candidate availability assessment, automation-first FEED architecture designed for 40 to 60% lower headcount than offshore equivalent, AI-native IT/OT engineering at 10 to 18% of CapEx, utility lead-time critical path planning, full TCO model with tariff and energy sensitivity scenarios, and net-zero ESG integration. All outputs delivered before land acquisition or financial close.

Book your US reshoring greenfield consultation here.