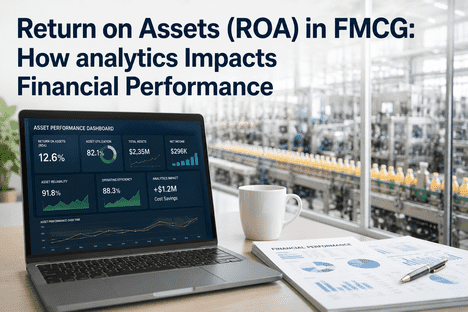

Return on Assets is one of the most closely watched financial metrics in FMCG manufacturing — and one of the most directly affected by equipment analytics. ROA measures how efficiently a company converts its asset base into net income, calculated as net income divided by total assets. For FMCG manufacturers, where production equipment represents 40–60% of total asset value and where annual capital expenditure on machinery routinely reaches 5–8% of revenue, even small improvements in asset productivity produce significant ROA expansion. A typical mid-size FMCG facility with $500M in total assets and $25M in net income operates at 5% ROA. A 20% improvement in equipment-driven net income — achievable through predictive maintenance, OEE optimization, and energy analytics — lifts ROA to 6%, representing a 20% relative improvement that directly affects the company's weighted average cost of capital, valuation multiples, and borrowing terms. This article provides the analytical framework connecting iFactory's equipment analytics capabilities to ROA improvement across three specific levers — asset utilization, maintenance cost reduction, and asset lifecycle optimization — with documented impact ranges from deployed facilities. Book a Demo to receive an ROA impact projection based on your facility's current asset base and financial data.

Understanding ROA in the FMCG Context

ROA = Net Income / Total Assets. The ratio tells the CFO how many dollars of profit each dollar of assets generates. In FMCG manufacturing, where margins are thin (5–12%) and asset intensity is high, ROA is a primary indicator of operational efficiency and a key input to the company's cost of capital calculation. A manufacturer with 4% ROA pays more for debt and equity capital than a peer at 7% ROA, creating a compounding disadvantage that affects every capital allocation decision.

The numerator — net income — is affected by every operational efficiency gain: higher OEE means more output per asset dollar, lower maintenance spend flows directly to operating margin, reduced energy consumption lowers cost of goods sold, and quality scrap reduction preserves material value. The denominator — total assets — is affected by asset lifecycle decisions: extending equipment life through predictive maintenance defers capital replacement, optimizing MRO inventory reduces current assets, and eliminating redundant spare assets through reliability improvement reduces gross asset carrying value. Most ROA improvement initiatives in FMCG focus exclusively on the numerator. The analytics-enabled approach addresses both sides simultaneously, producing ROA improvement that is 2–3× larger than income-only strategies.

Lever 1: Asset Utilization — Extracting More Income Per Asset Dollar

The most direct way analytics improves ROA is by increasing net income generated by the existing asset base — without adding new assets to the denominator. OEE analytics provides the mechanism: every percentage point of OEE improvement increases production output from the same equipment, effectively reducing the asset intensity of each unit produced.

iFactory's OEE Analytics module tracks availability, performance, and quality at the line and asset level, attributing losses to specific root causes — micro-stops, speed reduction, changeover delay, quality rejects — with enough granularity that reliability teams can target the highest-impact loss categories first. A facility operating at 65% OEE that improves to 78% — within the documented range for iFactory deployments — increases effective production capacity by 20% without capital expenditure. That capacity translates to $3–8M in additional annual output value in a typical mid-size FMCG plant, flowing directly to net income and improving ROA by 0.6–1.6 percentage points depending on asset base size.

Lever 2: Maintenance Cost Reduction — Improving the Numerator Directly

Maintenance spend is the second-largest controllable operating cost in most FMCG facilities after raw materials, typically representing 12–18% of total operating expenditure. In a facility with $200M in annual operating cost, that is $24–36M flowing through the P&L as a direct deduction from net income. Every dollar of maintenance cost reduction that does not compromise asset reliability flows dollar-for-dollar to net income — and analytics provides the mechanism to identify which maintenance dollars are value-creating and which are waste.

iFactory's predictive maintenance and work order management modules deliver three categories of cost reduction: (1) emergency repair elimination — reducing the 3–5× cost premium of reactive repairs versus planned interventions, (2) over-maintenance deferral — shifting calendar-based PM schedules to condition-based schedules that eliminate unnecessary PM tasks on assets that do not need them, and (3) labor productivity improvement — reducing the 2–4 hours per technician per week lost to administrative and search activities. The combined effect across all three categories is 18–25% total maintenance cost reduction. For the $30M maintenance budget example, a 20% reduction saves $6M annually — directly increasing net income by that amount and improving ROA by approximately 1.2 percentage points. Book a Demo to see a maintenance cost reduction projection for your facility.

Lever 3: Asset Lifecycle Optimization — Managing the Denominator

The denominator side of ROA — total assets — is often treated as fixed in the short term, but analytics-driven lifecycle management demonstrably reduces the asset base required to sustain production output. Four mechanisms contribute: (1) equipment life extension through predictive maintenance defers capital replacement, reducing the average asset base over time, (2) MRO inventory optimization reduces current assets by 20–30% without increasing stockout risk, (3) reliability improvement eliminates the need for redundant standby assets maintained "just in case," and (4) capital efficiency — capital is deployed to high-ROA projects instead of emergency replacements, improving the marginal return on each capital dollar.

The combined effect across these mechanisms reduces the asset denominator by 5–12% over 24–36 months without reducing production capacity — because the existing assets become more reliable and produce more output per unit of asset value. For a facility with $500M in total assets, a 7% reduction in the asset base ($35M) combined with a $6M net income improvement from maintenance cost reduction produces an ROA improvement from 5.0% to approximately 7.2% — a 44% relative improvement. This combined numerator-and-denominator effect is the defining financial advantage of analytics-driven asset management over purely operational improvement programs.

The Analytics-to-ROA Impact Framework

The table below maps each iFactory analytics capability to the specific ROA component it affects, the documented impact range, and the typical timeline to full financial effect. This framework is designed to support a capital allocation discussion with the CFO by connecting platform investment directly to the financial metric that governs the company's cost of capital.

| iFactory Analytics Capability | ROA Component Affected | Impact Mechanism | Documented Impact Range | Timeline to Financial Effect |

|---|---|---|---|---|

| OEE Analytics & Production Monitoring | Net Income (numerator) | Increased output from existing assets without capital spend; lower unit cost through fixed cost absorption | 8–15 OEE percentage points → 12–20% output gain | 3–9 months |

| Predictive Maintenance & EAM | Net Income (numerator) | Emergency repair elimination; planned vs. reactive cost ratio improvement; labor productivity gain | 18–25% maintenance cost reduction | 6–12 months |

| Energy Monitoring & Optimization | Net Income (numerator) | Direct utility cost reduction through consumption optimization, demand management, and baseline load elimination | 12–22% energy cost reduction | 3–9 months |

| Quality Control & SQC | Net Income (numerator) | Scrap and rework reduction; material yield improvement; restart waste elimination | 30–50% quality scrap reduction | 3–9 months |

| Parts & Inventory Optimization | Total Assets (denominator) | MRO inventory value reduction; emergency stock elimination; inventory turnover improvement | 20–30% MRO inventory reduction | 12–18 months |

| Enterprise Asset Management | Total Assets (denominator) | Equipment life extension; capital replacement deferral; redundant asset elimination | 20–40% asset life extension; 5–12% asset base reduction | 12–36 months |

| Analytics Reporting & Operational Dashboard | Both numerator & denominator | Sustains savings across all categories through visibility and accountability; prevents savings erosion | 85–95% savings retention at 18 months (vs. 40–60% without dashboards) | Ongoing |

Building the Analytics-to-ROA Business Case for Your CFO

The analytics-to-ROA framework enables a capital proposal structured around the metric the CFO already uses to evaluate the company's financial health. The business case follows a five-step sequence designed to align with corporate finance review processes.

Establish the Current ROA Baseline

Calculate the facility's current ROA using the most recent 12 months of financial data: net income / total assets. If the facility-level ROA is not separately reported, estimate it by applying the corporate ROA to the facility's proportionate asset base. This baseline is the reference point against which all analytics-driven improvement will be measured.

Quantify Numerator Impact from Maintenance & Energy Cost Reduction

Extract current maintenance spend, energy cost, and scrap rate from the P&L. Apply conservative reduction rates — 18% for maintenance (the low end of the documented range), 12% for energy, 30% for scrap. Multiply each by the current spend to calculate annual net income improvement. Sum these to produce the numerator-side ROA impact.

Quantify Denominator Impact from Inventory & Asset Optimization

Extract current MRO inventory value and gross equipment asset base from the balance sheet. Apply conservative reduction rates — 20% for MRO inventory, 5% for equipment asset base through life extension and deferred replacement. Calculate the total asset reduction and express it as a percentage of current total assets.

Calculate Combined ROA Improvement

Apply the net income improvement (numerator) and asset base reduction (denominator) to the baseline ROA. The combined effect — increased income divided by decreased assets — produces an ROA improvement that is significantly larger than either effect independently. Present this as the analytics-enabled ROA target with a timeline of 12–24 months to full realization.

Present Platform Investment Against ROA Impact

The total iFactory platform investment for a multi-line facility ranges from $85,000–$220,000 in Year 1. Compare this to the ROA improvement impact in basis points and to the market value of a one-basis-point ROA improvement for the company. When framed as the investment required to produce a specific, measurable ROA improvement — rather than as a technology purchase — the business case aligns with the CFO's capital allocation framework. Book a Demo to have iFactory's financial analytics team run this five-step model against your actual facility data.

The Three Financial Objections to Analytics Investment — Answered

The most common objections CFOs raise when presented with an analytics-for-ROA proposal follow a consistent pattern. Preparing specific responses to each strengthens the proposal and demonstrates financial rigor.

A 1.5-percentage-point ROA improvement at a facility with $500M in assets is $7.5M in additional annual net income from the same asset base. When applied across multiple facilities, the aggregate ROA improvement reaches the threshold that affects the company's weighted average cost of capital — reducing borrowing costs by 25–50 basis points for every full ROA percentage point gained.

Most FMCG facilities have not exhausted maintenance cost reduction potential through existing methods because the data required to distinguish value-creating PM tasks from unnecessary ones is not available without analytics. The 18–25% reduction range documented in iFactory deployments is additive to — not a substitute for — the 5–10% reduction achievable through conventional process improvement in the same facilities.

Condition-based maintenance extends the productive life of assets while actually reducing per-year maintenance cost — because interventions occur at the optimal point in the deterioration curve, not before or after. The analytics-enabled extension of equipment life from 15 to 18 years, for example, defers the $2M capital replacement cost for 3 years while maintaining or reducing annual maintenance spend through optimized intervention timing.

Conclusion: ROA Is the Metric That Connects Operations to Finance

Return on Assets is the financial metric that most directly connects operational performance to corporate financial health — and it is the metric most directly improved by equipment analytics. Unlike EBITDA or gross margin, ROA captures both the income-generating effect of operational efficiency (numerator) and the capital efficiency effect of asset lifecycle management (denominator). An analytics-enabled maintenance and production program improves both simultaneously, producing ROA improvement that conventional cost-reduction programs cannot match.

iFactory's integrated analytics platform provides the data infrastructure for both sides of the ROA equation: OEE analytics, predictive maintenance, energy monitoring, and quality control drive the numerator improvement; asset lifecycle management, inventory optimization, and capital efficiency analytics drive the denominator reduction. The combined 2–4 percentage point ROA improvement documented across iFactory deployments represents $10–20M in additional annual net income per $500M in assets — making the platform investment one of the highest-return capital allocation decisions available to an FMCG manufacturer. Book a Demo to see the ROA impact model run against your facility's asset base and financial statements.

Frequently Asked Questions

How quickly does analytics-driven ROA improvement appear in financial statements?

Numerator effects — maintenance cost reduction, energy savings, scrap reduction — appear in the P&L within 3–6 months of deployment. Denominator effects — MRO inventory reduction, asset life extension — require 12–24 months to fully materialize as assets are optimized and replacement cycles adjust. The combined ROA impact becomes measurable at the facility level within 9–12 months.

How is ROA improvement measured at the facility level when assets are shared across multiple facilities?

iFactory's analytics reporting module tracks ROA contribution at the facility level by attributing shared assets based on utilization hours and by allocating net income improvement through directly measurable cost reduction categories — maintenance spend, energy consumption, scrap rate, OEE — that are tracked at the line and asset level independently of corporate allocation methodology.

What ROA improvement can a single-facility deployment expect?

Single-facility deployments typically produce 0.8–2.5 percentage points of ROA improvement within 12–18 months, depending on the facility's current OEE baseline, maintenance cost structure, and deployment scope. Multi-facility deployments compound this effect through enterprise-wide standardization, typically reaching 2–4 percentage points of improvement across the enterprise.

Does iFactory provide the ROA calculation within the platform, or do we need to compute it separately?

iFactory's operational dashboard integrates with your ERP and financial systems to track the specific cost and asset data inputs required for ROA calculation — maintenance spend, energy cost, scrap value, output value, MRO inventory, asset register — and presents them in a format that enables facility-level ROA tracking without requiring additional financial analysis tools.

How does ROA improvement from analytics affect the company's cost of capital?

Credit rating agencies and institutional investors use ROA as a key input to cost of capital calculations. A sustained 1-percentage-point ROA improvement typically reduces the weighted average cost of capital by 25–50 basis points for a mid-size FMCG manufacturer — reducing borrowing costs by $500,000–$1,500,000 annually per $500M in debt, creating a compounding financial benefit beyond the direct operational savings.