The Governmental Accounting Standards Board is rewriting the rules of infrastructure asset reporting. The April 2026 Exposure Draft proposing amendments to GASB Statement No. 34 introduces mandatory component-level depreciation, required periodic reassessment of useful lives and salvage values, and expanded disclosure requirements for aging assets that have exceeded 80 percent of their estimated useful lives. For asset managers and finance officers managing multi-billion-dollar infrastructure portfolios, the proposed standard represents the most significant shift in governmental infrastructure accounting since GASB 34 was issued in 1999. The deadline for comment on the Exposure Draft is June 26, 2026, with the final standard expected by mid-2027 and an effective date for fiscal years beginning after June 15, 2028. The organisations that begin preparing now — by auditing their current useful life assumptions, evaluating componentization requirements, and deploying AI-driven condition assessment platforms — will transition ahead of the curve and avoid the restatement shocks that retroactive application will create for those who wait.

1999

GASB Statement No. 34 established infrastructure asset reporting requirements — the 2026 Exposure Draft is the most significant revision in 27 years

FY 2029

Proposed effective date for the new infrastructure standard — fiscal years beginning after June 15, 2028, with earlier adoption encouraged

80%

New threshold for aging asset disclosures — infrastructure assets exceeding 80 percent of estimated useful life require network-level reporting

USD 1T

Estimated deferred maintenance backlog across US government infrastructure — AI condition scoring provides the defensible data GASB now requires

The GASB Infrastructure Standard Is About to Change. Your Asset Data Determines Whether You Lead or React.

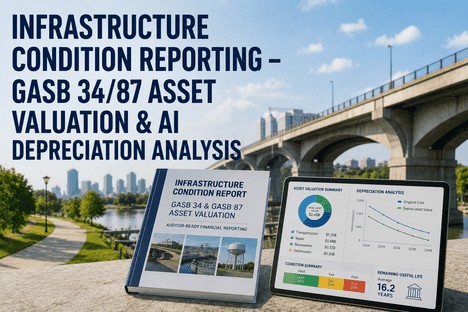

iFactory's AI-driven condition assessment platform generates the asset valuation data, depreciation analytics, and useful life projections that GASB 34/87 compliance requires — with auditor-ready reports and continuous condition scoring that turns regulatory obligation into capital planning intelligence.

GASB 34 and GASB 87 — The Two Standards That Define Infrastructure Asset Reporting

Asset managers responsible for governmental infrastructure reporting operate under two distinct but interconnected GASB standards. GASB Statement No. 34 governs how infrastructure assets are recognised, depreciated, and disclosed in financial statements. GASB Statement No. 87 governs lease accounting for right-to-use assets — including infrastructure assets leased by or to government entities. The proposed 2026 amendments to GASB 34 introduce requirements that will affect both frameworks by demanding more granular asset-level data, condition-adjusted valuations, and network-level disclosure. Understanding both standards is essential for any asset manager preparing for the transition.

Requires infrastructure assets to be reported at historical cost net of accumulated depreciation or using the modified approach for eligible assets

The modified approach requires condition assessments at least every three years and documented preservation expenditures meeting a defined condition level

2026 Exposure Draft proposes mandatory component-level depreciation when a component cost is significant and its useful life substantially differs from the main asset

Proposed standard requires periodic reassessment of estimated useful lives and salvage values with retroactive restatement for misstated prior depreciation

New disclosures by network: historical cost weighted-average age for assets exceeding 80 percent and 100 percent of estimated useful lives

Proposed Effective Date: Fiscal years beginning after June 15, 2028 | Comment deadline: June 26, 2026

GASB 87

Leases — Right-to-Use Asset Accounting for Governments

Establishes a single model for lease accounting based on the principle that leases are financings of the right to use an underlying nonfinancial asset

Requires lessees to recognise a lease liability and an intangible right-to-use lease asset for all leases with a term longer than 12 months

Requires retroactive application — existing leases must be recognised and measured based on facts and circumstances at the date of implementation

Excludes SBITAs (GASB 96) and short-term leases under 12 months; PPPs and availability payment arrangements covered by GASB 94

GASB 87 intersects with GASB 34 where leased infrastructure assets must be reported under both standards — lease liability under 87, asset condition under 34

Effective for fiscal years beginning after June 15, 2021 | Retroactive application required for all existing leases

What the 2026 GASB Infrastructure Assets Exposure Draft Changes — A Visual Timeline

The proposed amendments to GASB 34 follow a structured timeline from comment period through to mandatory adoption. Asset managers who understand each phase and its documentation requirements will be positioned to transition efficiently rather than scrambling to reconstruct years of asset condition data when the standard takes effect.

Jun 2026

Phase 1 — Public Comment Period

Exposure Draft Review and Stakeholder Feedback

GASB issued the Infrastructure Assets Exposure Draft on April 8, 2026, with a comment deadline of June 26, 2026. Asset managers should submit feedback on proposed componentization thresholds, useful life reassessment requirements, and network-level disclosure scope. Early engagement with the proposed language allows asset managers to influence the final standard and begin internal gap analysis against current data systems.

Mid 2027

Phase 2 — Final Standard Issued

GASB Board Deliberations and Final Statement Publication

After reviewing comment letters and conducting board deliberations, GASB is expected to issue the final standard by mid-2027. Asset managers should use the period between comment closing and final issuance to perform a preliminary useful-life audit across infrastructure portfolios, assess current componentization practices, and evaluate whether existing asset management systems can generate the network-level aging data the new standard will require.

FY 2029

Phase 3 — Mandatory Adoption

Effective for Fiscal Years Beginning After June 15, 2028

The new standard applies to fiscal years beginning after June 15, 2028, with earlier adoption encouraged. At adoption, asset managers must reassess estimated useful lives and salvage values for all infrastructure assets held at the beginning of the reporting period. Any adjustments from the reassessment are reported retroactively by restating beginning net position. The expanded disclosures for aging assets — by network, with historical cost weighted-average age — apply beginning in the first reporting period of implementation.

Ongoing

Phase 4 — Continuous Compliance

Ongoing Condition Assessment, Depreciation Review, and Network-Level Disclosure

Post-adoption, asset managers must maintain continuous compliance through periodic reassessment of useful lives, ongoing condition assessments for assets using the modified approach, and annual network-level disclosures. iFactory's AI-driven platform automates this continuous compliance cycle — generating condition-adjusted depreciation schedules, flagging assets approaching the 80 percent threshold, and producing auditor-ready network-level disclosure reports from operational data captured at the point of inspection.

Your Infrastructure Assets Are Aging. Your GASB Disclosure Requirements Are Expanding. AI Is the Bridge.

iFactory's AI condition scoring engine generates daily-updated health scores for every infrastructure asset, automatically calculates remaining useful life and depreciation adjustments, and produces the network-level aging disclosures the new GASB standard will require.

The Four Compliance Mandates in the Proposed Standard — and What Each Requires From Your Asset Data

The GASB Infrastructure Assets Exposure Draft introduces four distinct compliance mandates that together represent a fundamental shift in how infrastructure assets must be tracked, valued, and disclosed. Each mandate places new demands on the quality, granularity, and continuity of asset data — demands that manual inspection and spreadsheet-based asset registers cannot meet at portfolio scale.

Component-Level Depreciation

Identify components where cost is significant relative to total asset cost and useful life is substantially different from the main asset

Depreciate each qualifying component separately with its own useful life and salvage value

Example: a road's surface course with 15-year life treated separately from roadway base with 40-year life

AI Requirement: Automated component identification from asset registry data and condition history

Useful Life Reassessment

Periodically review estimated useful lives and salvage values for all infrastructure assets reported at historical cost

Adjust accumulated depreciation retroactively when reassessment indicates prior depreciation was misstated

Report adjustments by restating beginning net position for the earliest period presented

AI Requirement: Continuous condition-based useful life modelling from inspection and sensor data

Aging Asset Disclosures

Disclose by network: historical cost, accumulated depreciation, and weighted-average age for assets exceeding 80 percent of useful life

Separate assets reaching 100 percent of useful life from those exceeding 80 percent but not yet at 100 percent

Describe the government's policy for monitoring maintenance and preservation of infrastructure assets

AI Requirement: Automated aging reports by network with real-time threshold tracking

Modified Approach Expansion

Condition assessment comparison period expanded from 5 to 10 reporting periods, presented by infrastructure network

Document that assets are being preserved at or above the defined condition level through preservation expenditures

Assets with zero reactive events in 12 months may indicate over-maintained intervals for optimisation

AI Requirement: Condition trend analytics with 10-year preservation expenditure correlation

How AI-Driven Condition Assessment Transforms GASB Compliance — Four Capabilities Every Asset Manager Needs

AI-powered infrastructure condition assessment is not a faster version of manual inspection reporting. It is a fundamentally different data architecture: continuous rather than periodic, predictive rather than descriptive, and fully integrated with the financial reporting systems that produce GASB-compliant disclosures. For asset managers preparing for the 2028 transition, these four AI capabilities directly address the new standard's core requirements.

Capability 01

Continuous AI Condition Scoring for Every Infrastructure Asset

Asset Valuation

iFactory's AI engine calculates a daily condition score for every infrastructure asset by processing inspection records, sensor data, maintenance history, material age and specification data, environmental exposure factors, and usage load profiles. The scoring model is calibrated per asset class — a bridge deck's score weights structural inspection findings and traffic load differently from a water treatment plant's score, which weights runtime hours and chemical exposure. Each asset receives a 0-to-100 health score updated continuously, not just during inspection cycles. This continuous scoring provides the condition-adjusted remaining useful life data that GASB's proposed useful life reassessment mandate requires — replacing static age-based depreciation schedules with dynamic valuations that reflect actual asset condition.

Capability 02

Automated Depreciation Analysis With Condition-Adjusted Useful Life Modelling

Depreciation Analysis

The proposed GASB standard's requirement for periodic reassessment of estimated useful lives and salvage values demands a level of asset intelligence that traditional depreciation schedules cannot provide. iFactory's platform generates condition-adjusted depreciation curves for every infrastructure asset — calculating remaining useful life not from a fixed calendar assumption but from the asset's actual condition trajectory as measured through continuous scoring. When the AI detects that an asset's deterioration rate is accelerating or decelerating relative to its original useful life estimate, the platform flags the variance and calculates the retroactive depreciation adjustment that the new standard will require at adoption. For asset managers facing the transition, this means entering the FY 2029 adoption with a defensible, data-backed useful life reassessment rather than a retrospective estimate that auditors will challenge.

Capability 03

Network-Level Aging Asset Tracking and Disclosure Report Generation

Disclosure Automation

The proposed standard's most operationally significant disclosure requirement is the network-level reporting of aging assets — historical cost weighted-average age for infrastructure assets that have exceeded 80 percent of their estimated useful lives, with separate disclosure for assets reaching 100 percent. iFactory's reporting engine organises every asset by network classification (road network, water system, bridge inventory, building portfolio) and tracks each asset's current age against its AI-calculated useful life projection. When an asset crosses the 80 percent threshold, the platform flags it for disclosure and includes it in the network-level aging report. At reporting period close, the compliance officer generates the network-level disclosure report with a single action — populated with current data, calculated to the standard's format requirements, and linked to the underlying condition assessment records that auditors will request for verification.

Capability 04

Modified Approach Documentation With 10-Year Preservation Expenditure Correlation

Modified Approach

For governments using the modified approach to avoid depreciation on eligible infrastructure assets, the Exposure Draft expands the required supplementary information comparison period from 5 to 10 reporting periods, presented by infrastructure network. This means asset managers must maintain 10 years of condition assessment data and preservation expenditure records, organised by network, demonstrating that assets are being preserved at or above the defined condition level. iFactory's platform maintains this data automatically — every condition score, every preservation expenditure, every inspection record is stored with a network classification and timestamp. When the RSI schedule is due, the platform generates the 10-year comparison directly from stored data, eliminating the manual reconstruction that would otherwise consume weeks of staff time for each reporting cycle.

Our city manages over 4,700 infrastructure assets across six networks — roads, bridges, water distribution, wastewater collection, stormwater systems, and public buildings. When we modelled the impact of GASB's proposed componentization requirements on our current reporting, we discovered that 340 of our assets would require component-level depreciation treatment, and our existing age-based depreciation schedules would produce materially misstated accumulated depreciation for roughly 60 percent of those assets. Without AI-driven condition scoring, the workload of reassessing useful lives and reconstructing component-level records across 4,700 assets would have required three full-time staff working for eighteen months. With iFactory's platform, we completed the initial condition baseline in eight weeks. The platform now generates our network-level aging disclosures on demand, and our auditor has confirmed that the condition-adjusted depreciation curves meet the proposed standard's evidentiary requirements.

— Director of Asset Management, Municipal Public Works Department — 500,000+ Service Population, 24 Years Infrastructure Management Experience

Conclusion — The GASB Infrastructure Standard Is Changing Whether You Are Ready or Not. The Question Is How Much of the Transition You Automate.

Infrastructure asset managers face a clear choice as the GASB Infrastructure Assets Exposure Draft moves toward finalisation. The option of continuing with current documentation practices until the standard takes effect in FY 2029 is understandable — but it is also the option that leads to the most disruptive transition. Retroactive useful life reassessment across thousands of assets, component-level depreciation reclassification, network-level aging disclosures reconstructed from incomplete records, and modified approach RSI expanded from five to ten years of data — each of these requirements becomes exponentially harder to implement if asset data is not already being captured in the right format, at the right granularity, with the right condition context.

The agencies that will transition smoothly are those that begin now — conducting preliminary useful-life audits on their current infrastructure portfolios, evaluating whether their existing asset management systems can produce component-level depreciation schedules and network-level aging reports, and deploying AI-driven condition assessment platforms that generate the continuous asset intelligence the new standard will demand. With the comment deadline set for June 26, 2026, the final standard expected by mid-2027, and mandatory adoption for fiscal years beginning after June 15, 2028, the window for proactive preparation is closing. Every year of asset data captured on an AI-powered condition scoring platform before adoption is a year of defensible evidence that auditors cannot challenge and that GASB's new disclosure requirements will recognise.

iFactory's AI infrastructure condition assessment platform gives asset managers the continuous condition scoring, automated depreciation analysis, network-level aging reports, and modified approach documentation that GASB 34/87 compliance demands — with auditor-ready outputs and a data architecture designed for the new standard's componentization and useful life reassessment requirements. Book a Demo to see how the platform maps to your infrastructure portfolio's specific GASB compliance requirements, or talk to an expert about conducting a preliminary useful-life audit on your current infrastructure asset data before the standard takes effect.

Frequently Asked Questions

Under the historical cost approach, infrastructure assets are recorded at their acquisition cost and depreciated over their estimated useful lives using a straight-line or composite method. Accumulated depreciation is reported on the statement of net position, and depreciation expense is recognised each reporting period. Under the modified approach, eligible infrastructure assets are not depreciated — provided the government meets two conditions: (1) the assets are managed using an asset management system with up-to-date condition assessments conducted at least every three years, and (2) the government documents that the assets are being preserved at or above a defined condition level. The 2026 Exposure Draft expands the modified approach's RSI comparison period from 5 to 10 reporting periods and requires network-level presentation. Governments that cannot demonstrate they meet both conditions must use historical cost depreciation. iFactory supports both approaches with automated condition scoring for modified approach documentation and condition-adjusted depreciation schedules for historical cost reporting. Book a demo to see which approach fits your portfolio.

iFactory's AI engine processes up to eight condition inputs per asset class — inspection findings, sensor data streams, maintenance history, material age and specification, environmental exposure, usage load, repair frequency, and failure patterns — to generate a dynamic remaining useful life estimate for every infrastructure asset. Unlike age-based depreciation that assumes uniform deterioration over time, iFactory's model reflects actual condition trajectory: an asset that has been well-maintained in a low-stress environment will show a longer remaining useful life than the same asset type in a high-stress environment with deferred maintenance. When the proposed GASB standard takes effect, this condition-adjusted remaining useful life data provides the defensible basis for the required periodic useful life reassessment. The platform also calculates the retroactive depreciation adjustment that would result from changing the useful life assumption — giving asset managers a pre-implementation estimate of the beginning net position restatement that adoption will require. Talk to an expert about running a preliminary useful-life audit on your portfolio.

Under the proposed Exposure Draft, governments using historical cost depreciation must disclose by network of infrastructure assets: (1) historical cost, (2) accumulated depreciation, and (3) historical-cost weighted-average age for two categories of aging assets — those that have reached 100 percent of their estimated useful lives, and those that have exceeded 80 percent but have not yet reached 100 percent. iFactory's reporting engine tracks every infrastructure asset against its AI-calculated useful life projection, automatically classifying assets into the 80-to-100 percent and 100-plus percent categories. The network-level disclosure report is generated with current data at each reporting period close, eliminating the manual process of filtering asset registers by age categories and calculating weighted-average age across thousands of assets. The platform also alerts asset managers when any infrastructure asset crosses the 80 percent threshold during the reporting period — enabling proactive disclosure planning rather than retroactive data compilation. Book a demo to see the aging asset disclosure report generated from your infrastructure data.

iFactory's integration layer connects with GIS platforms (ESRI ArcGIS, QGIS), CMMS systems (IBM Maximo, SAP EAM, Infor EAM), and financial management systems (Oracle E-Business Suite, SAP S/4HANA, Microsoft Dynamics) through REST APIs and direct database connectors. Asset registers are synchronised automatically — when a new asset is added to GIS, it appears in iFactory's condition scoring engine within the same sync cycle. Inspection data from mobile field apps flows into the platform and updates the asset's condition score immediately. Financial system data on capital costs and accumulated depreciation is pulled into the GASB reporting module for reconciliation with condition-adjusted valuations. The platform does not require migration away from existing operational systems — it serves as the unified data layer that connects operational asset data to financial reporting outputs. Talk to an expert to review your current system architecture and confirm integration compatibility with iFactory's GASB compliance module.

Five actions are immediately actionable. First, conduct a preliminary useful-life audit — compare your current assigned useful lives against observed asset condition data to quantify the potential restatement magnitude. Second, evaluate your current asset registry for componentization requirements — identify infrastructure assets where components have significantly different useful lives and assess whether your current system can track them separately. Third, assess your network-level data organisation — the proposed standard requires disclosure by network, and many agencies do not currently classify assets by network in their financial reporting systems. Fourth, expand your condition assessment frequency — the modified approach requires triennial minimum assessments, but continuous AI-driven scoring will provide a stronger evidentiary basis for both the historical cost and modified approach methods. Fifth, submit comments to GASB before the June 26, 2026 deadline — stakeholder feedback directly shapes the final standard's thresholds and implementation requirements. Book a demo to discuss these five preparatory actions with iFactory's infrastructure asset management team and see how the platform supports each one with automated data collection and analysis.

The GASB Infrastructure Standard Has a Timeline. Your Asset Data Needs to Be Ready Before the Clock Runs Out.

iFactory's AI-powered condition assessment platform gives infrastructure asset managers the continuous scoring, automated depreciation analysis, network-level aging reports, and modified approach documentation that the new GASB standard will require — with auditor-ready outputs and a data architecture designed for the transition.